Bounce to winners | Soar to methodology

Prime boutiques flourishing in a complex tax regulation sector

Standing out in the aggressive location of tax legislation is always a problem. Even so, this year’s Prime Tax Regulation Boutiques not only served their clients with excellence and professionalism, but they have also been planning for and monitoring impending regulatory variations.

Tara Benham, countrywide tax leader at Grant Thornton, spelled out that the real check of remaining a standout business is “being acknowledged by customers, accountants, and other legal professionals for their expertise”.

All Canadian Law firm’s 10 greatest-in-class tax boutiques, the fifth version, drew rave opinions from study respondents who integrated referring corporations, clients, and personnel.

“[Tax complexity] will have an affect on the very long-term advancement fee of persons in the market and that’s heading to be a pattern to maintain an eye on in excess of the up coming several years”

Alexander Demner, Thorsteinssons LLP

Alexander Demner, Thorsteinssons LLP

Tax regulation companies: Industry insight

Thorsteinssons LLP, with places of work in Toronto and Vancouver, has extended held the name as one of Canada’s leading tax law companies, as evident from the perception available by Canadian Lawyer’s study respondents. Their responses integrated:

• “Simply the most effective tax lawyers”

• “Well-acknowledged specialists”

• “Top-tier tax lawyers”

• “They have the best bench power in the country”

Other good reasons provided by field insiders for the firm’s good results have been “the dimensions and scope of practice” and “their wide tax observe,” when a survey respondent discussed it was simply because of “their superb depth and superior tax litigation”.

Fellow awardee Morris Kepes Winters LLP was cited for “their 20-12 months historical past as a tax boutique in the SME space”. An additional respondent highlighted the firm’s skill to “provide equally tax organizing and tax litigation” and 1 consumer commented, “I identified the overall expertise of their lawyers and the do the job exceptional”.

Other good reasons the Toronto-primarily based firm stood out among the its peers were:

• “Strong companions who exhibit a purchaser-centric approach”

• “Very professional and proficient practitioners”

• “Great litigators”

And their client, tailor made house builder Walden Households, explained that the company “has a quite strong knowledge of our business and offers inventive solutions”.

Millar Kreklewetz LLP was praised for carving out a beneficial area of interest for clients and partners. The agency, which opened in 1991, was cited for:

• “Specializing in commodity and profits taxes”

• “Specializing in customs and trade law”

• “Expertise in commodity law”

“The complexity and deficiency of clarity in these proposed (obligatory disclosure) guidelines are relatively shocking”

Robert Winters, Morris Kepes Winters LLP

Robert Winters, Morris Kepes Winters LLP

Crucial to the firm’s award-winning position is its capability to supply realistic solutions for intricate difficulties. The business has educated attorneys who now direct oblique tax tactics at some of the country’s biggest legislation and accounting firms. Other respondents branded them “excellent lawyers” and suppliers of “the most effective commodity tax advice”.

Found in the heart of Toronto’s fiscal centre, TaxChambers LLP has also been acknowledged in the Best 10 Tax Law Boutiques. It is a compact follow that attracts clientele with its on-demand from customers teams and is regarded for its 3 distinctive strains of tax products and services: litigation, preparing and implementation, and US tax advisory.

Two of TaxChambers’ attorneys had been individually cited by sector authorities as the motive why they operate with them:

• “David Piccolo is a genius”

• “[The firm has] very expert and well-informed tax counsel. Vern Krishna, in distinct, is an skilled in income tax matters”

An additional respondent additional, “They supply excellent strong assistance and service”.

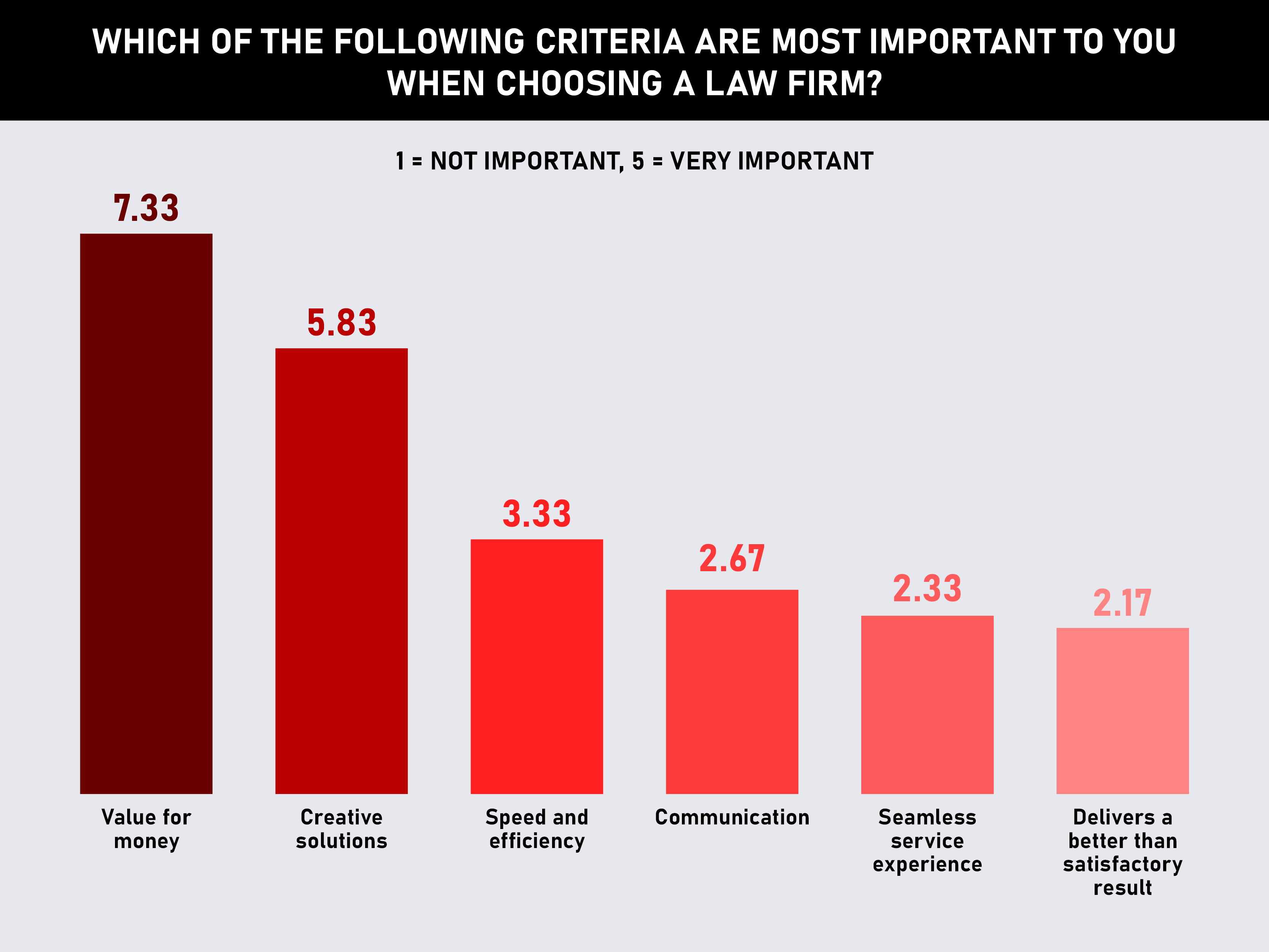

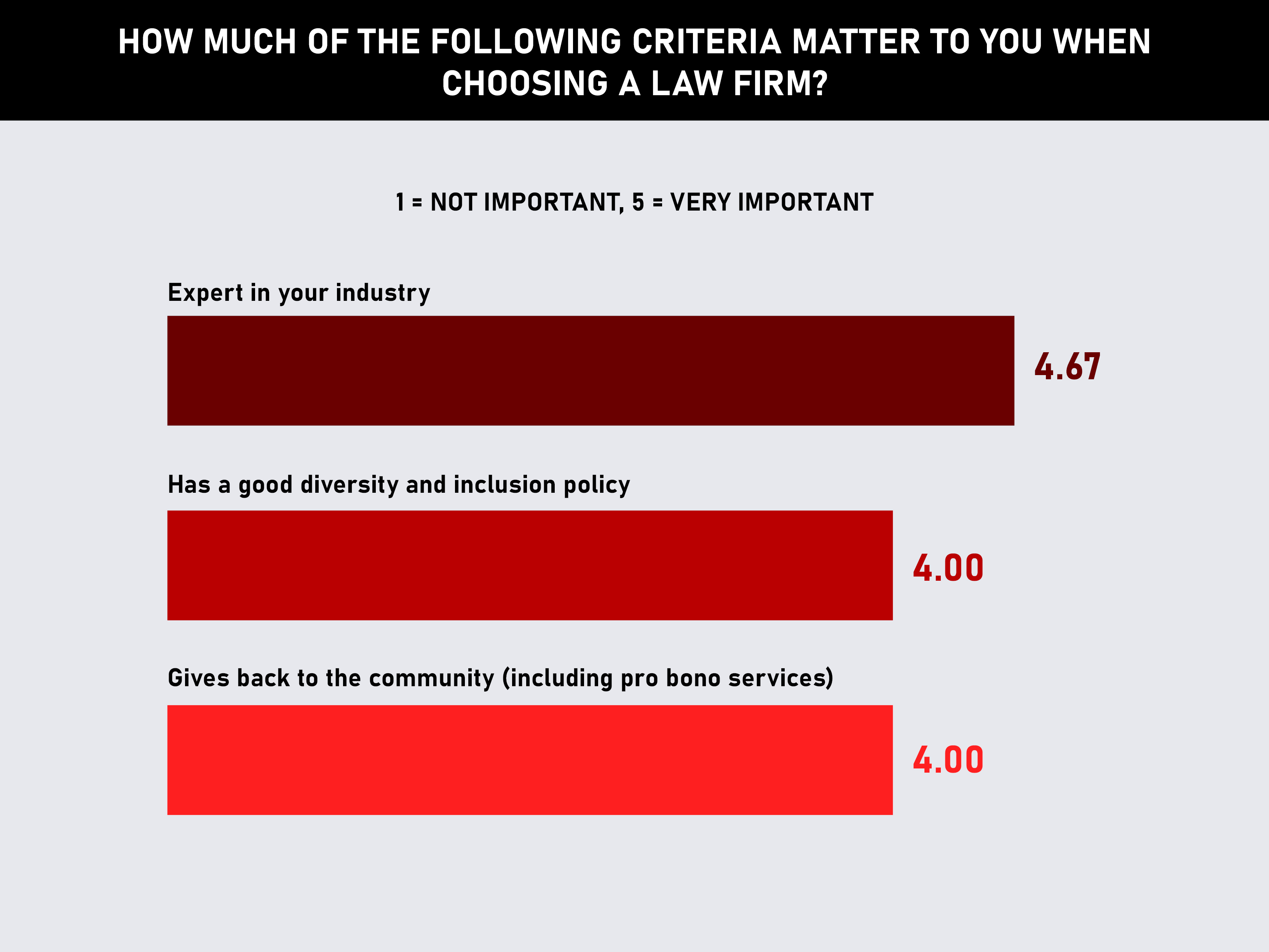

Worth attraction of tax legislation companies

As aspect of Canadian Lawyer’s study, respondents ended up asked to identify the decisive element in deciding on a company.

Legal professionals opened up on why price for funds is the most crucial factor. What is distinct is that it is not about being less expensive but supplying a improved package relative to price.

• “McDonald’s is the largest cafe in the planet, but it doesn’t make the best burger. Smaller boutiques do not have to cave to billing strain and can provide far more pro bono work and be far more price tag effective”

• “Specialized knowledge and better working experience generate additional value-efficient results”

• “Greater matter subject abilities without having the quality pricing”

“As a tax law firm, we’re frequently battling the government’s try to tax, so it’ll be more function for us, and a lot more challenges for common individuals out there and compact- to medium-sized businesses”

Robert Kreklewetz, Millar Kreklewetz LLP

Robert Kreklewetz, Millar Kreklewetz LLP

A storm is brewing for tax regulation companies

As the main exponents in their subject, the prime tax legislation boutiques are laying the groundwork for the federal government’s proposed laws all around obligatory disclosure regulations.

Aimed at helping the Canada Profits Company (CRA) clamp down on what it views as aggressive tax planning methods, the amendment to the Cash flow Tax Act would need lawyers and other advisors, in addition to the taxpayer, to report notifiable transactions.

“It’s fairly apparent that regardless of the professed wish from each individual stakeholder imaginable to simplify the tax code, it is decidedly going in the other direction,” suggests Alexander Demner, a companion in the Vancouver business of Thorsteinssons. “It will have an effect on the long-term growth level of individuals in the marketplace, and that is likely to be a pattern to continue to keep an eye on around the subsequent a number of several years.”

Robert Winters, a husband or wife at Morris Kepes Winters, calls the recommended rule-modify routine “relatively Draconian”.

The firm’s attorneys have many years of experience as tax litigators and tax planners. That knowledge provides them the complex experience required to advocate for consumers in disputes with the CRA and to stand for customers prior to the courts.

“The complexity and absence of clarity in these proposed principles are relatively shocking,” claims Winters. “It’s heading to be notably difficult on more compact legislation firms and other advisors that may perhaps not have the information or sophistication to deal with or entirely fully grasp their obligations.”

In short, Winters notes that the European Union Court docket of Justice (EUCJ) in December 2022 dominated against a case, which requires taxpayers and other intermediaries, including attorneys, to report specified cross-border tax setting up arrangements to governmental authorities.

“Canadian legislation has extremely robust safety for solicitor-shopper privilege,” says Winters. “The EUCJ decision was prompted by a obstacle from lawyers’ specialist companies in Belgium. It would look to provide a roadmap for very similar worries from Canadian regulation societies.”

Tax regulation firms’ silver lining

By most accounts, 2023 and outside of are predicted to be what tax and trade attorney Robert Kreklewetz of Millar Kreklewetz calls “up years”.

“I really do not see how the government can preserve investing the funds they are spending without the need of also placing a load on the taxes, which implies amplified taxes,” he points out. “As a tax lawyer, we’re usually fighting the government’s attempt to tax, so it’ll be a lot more operate for us, and much more challenges for common people out there and tiny- to medium-sized companies.”

When taxpayers are faced with a tax assessment, it’s like a no-gain problem, remarks Kreklewetz.

“You’ve got to struggle it it normally takes time, funds, and human psychological anxiousness to get as a result of all that to have your working day in court docket or get accessibility to justice,” he suggests. “A combat with the CRA is like getting in a smaller area with an elephant. The CRA is the elephant, and they’ve received the Office of Justice right there with them. So, you have received two elephants, and any way they switch, you have bought to be staying away from them.”

In accordance to Vitaly Timokhov, a partner at Toronto’s TaxChambers, the tax system works properly over-all.

“It’s a nutritious competition in a way,” he states, of the tug-of-war in between taxpayers’ financial very well-being and wealth and the government seeking to obtain as considerably revenue as doable in the legal framework.

Intergenerational transfers of small organization shares are best of thoughts for Timokhov, and his would like for the long term is that the federal authorities focuses on developing a a lot more friendly natural environment for that to happen.

All that staying explained, Victoria, BC-based mostly Dwyer Tax Legislation companion Blair Dwyer contends it’s turning out to be far more hard to give individuals tips they can depend on.

“The craze had been to try to make it so that folks understood the guidelines, but now we appear to be to be likely the opposite way, again to a process where by there seems to be an awful large amount of discretionary electrical power just due to the fact the provisions are so unclear,” states Dwyer.

“That’s a threat, men and women are likely to eliminate faith in the process because it is so complex and tricky to comply,” he provides.

The lawyers at Dwyer Tax have long and assorted working experience. They get the job done closely with their clients’ other advisers to acquire principled solutions tailored to the condition at hand. By involving the other advisers, the outcome is far more likely to address the lengthy-term demands of the consumer.

- Barsalou Lawson Rheault LLP

- Counter Tax Litigators

- Felesky Flynn LLP

- Legacy Tax + Have confidence in Lawyers

- Millar Kreklewetz LLP

- Moodys Tax Law

- Morris Kepes Winters LLP

To qualify, firms had been necessary to derive at least 80 percent of their function from tax law and have far more than one lawyer in this apply space. In complete, 189 ballots were obtained, casting votes for 14 candidates on Canadian Attorney’s listing. Final rankings ended up established via a points process in which companies had been rewarded on a sliding scale for the quantity of initial-to-tenth-area votes obtained. Voters had to rank a bare minimum of five companies.